Editor's Note: This is a long but important read. We know this is a complicated issue with many complex factors at play. If you still have questions after reading this article, email us at [email protected], and we'll do our best to answer them.

In light of the public hearings on the Bulloch County Schools (BCS) millage rate increase, Grice Connect has pulled together resources to help the community better understand how the Bulloch County Schools budget works.

In this article, you will find answers to these questions:

- How does Georgia fund school? (Video)

- How is the BCS budget organized?

- Can the school system's spending be audited?

- What is a local option sales tax (LOST)?

- What is an education special purpose local option sales tax (ESPLOST)?

- What is the difference between a LOST and an ESPLOST?

- What is a millage rate?

- What are the millage rates for recent years?

- How does the school system calculate the millage rate, and what does LOST have to do with it?

- What brings us to the current budget situation?

- What's next for Bulloch County Schools?

How does Georgia fund schools?

First, check out this video from the nonpartisan Georgia Budget & Policy Institute to see how Georgia schools are funded from the top down.

How is the BCS budget organized?

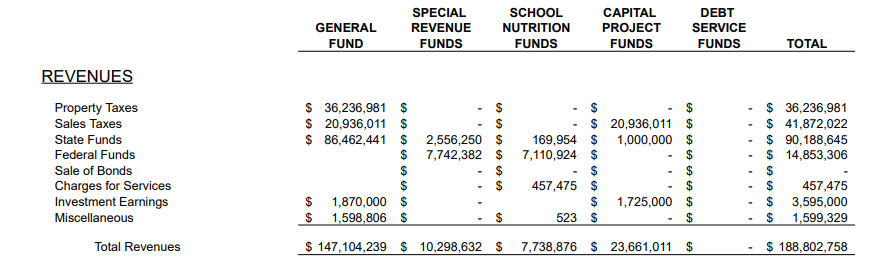

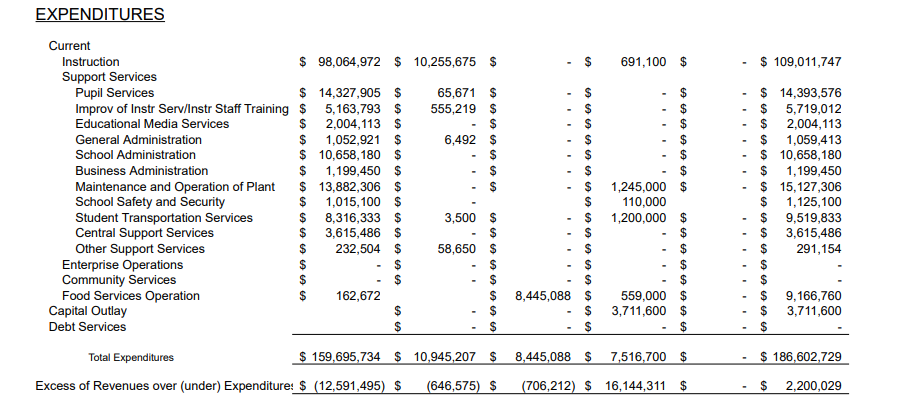

The overall budget includes five funds: General Fund, Capital Projects Fund, Special Revenue Fund, School Nutrition Fund, and Debt Service Fund.

Revenues in the budget include property taxes, sales taxes, state funds, federal funds, sale of bonds, charges for services (like school lunch), investment earnings, and miscellaneous revenues.

Not all streams of revenue can be used for all expenditures. See additional details from the FY26 budget below.

As you can see in the figure above, property taxes (determined by the millage rate) go toward the General Fund only, which is broken down into a variety of expenditures. Sales taxes (more on those below) go to both the General Fund and Capital Project Funds.

Continue down the columns below to see the expenditures and which category they fall into.

Can the school system's spending be audited?

Yes; the Bulloch County Board of Education's financial statements of governmental activities and each major fund of the school district are independently audited every year by the Georgia Department of Audits and Accounts. The Georgia Department of Audits and Accounts is an independent state agency that exists to provide independent, credible audit services promoting improvement in government.

Here's a six-year audit history for Bulloch County Schools:

- Annual Financial Report 2024

- Annual Financial Report 2023

- Annual Financial Report 2022

- Annual Financial Report 2021

- Annual Financial Report 2020

- Annual Financial Report 2019

The most recent audit report had no financial or federal findings reported, and this has been the case at Bulloch County Schools for more than 20 years. In fact, BCS was one of only 25 school districts to receive the Georgia Department of Audits & Accounts' Award of Distinction for Excellent Financial Reporting for Fiscal Year 2024 audits. It has won this award multiple times.

The school district also has the highest credit rating of AA+ from Standard & Poor's due to its proven sound financial practices. This rating allows the school district to obtain a lower interest rate on bonds when funding capital improvements, which saves both the district and taxpayers money.

You can click here to view a wide variety of financial accountability data from the school system, including salary scales. Note that Bulloch County Board of Education members do not receive a traditional salary. They each receive a $100 stipend for each meeting they attend, which is recorded as "Board Member Payroll" in the agenda packets here.

What is a local option sales tax (LOST)?

A local option sales tax is used to fund education in the county where it's collected. According to Georgia law, the money the county collects from the Local Option Sales Tax must be used to roll back the applicable county and school millage rates. You can see the amount collected that must be used here.

What is an education special purpose local option sales tax (ESPLOST)?

ESPLOST is a 1 cent sales tax used for funding special capital projects in the school system. ESPLOST does not fund the General Fund for BCS. It funds the construction of new schools and related costs inside of the Capital Projects Fund.

According to BCS, ESPLOST currently funds the capital-nature expenditures that have been moved from the General Fund to the Capital Projects Fund, alleviating approximately 2 mills worth of tax off of the General Fund.

Since 2003, the Board of Education has motioned to put an ESPLOST referendum on an election ballot for Bulloch voters. Recently, the BOE decided to place the next ESPLOST on the ballot in November.

The ESPLOST helps reduce the need for increasing property taxes or future millage rate increases, because it is an additional revenue stream for the school system. It also allows all people who shop in Bulloch county to share the tax burden. This may even include people who don't live here but do spend here. In other words, both property and non-property owners are helping to pay via ESPLOST.

As an example, funds generated from ESPLOST V are outlined to be used only in the following categories: Safety and Security; Instructional and Technology Resources; Building and Land; Equipment and Vehicles; Interest Expense and Miscellaneous Bank Fees. See additional details from the resolutions below.

(i) Safety and Security to include, but not limited to equipment and software, i.e., cameras, radios, lighting, fencing, fire suppression, security walls and glass, intercoms, bells, clocks, entry systems, networking, etc.;

(ii) Instructional and Technology Resources to include textbooks and other related materials; digital resource to include eBooks, subscriptions, etc.; software to include but not limited to license agreements, purchased software, or cloud based applications; and digital resource platforms to include but not be limited to license agreements, purchased platforms, or cloud based application; technology hardware and other devices;

(iii) Buildings and Land to include physical education (PE) and athletic facility improvements, renovations and additions; renovations, building and land improvements, and new construction to include but not be limited to roofing, plumbing, electrical, lighting, wiring, fiber, painting, water piping, HVAC, renovations necessary to comply with the Americans with Disabilities Act (ADA), energy management systems, repaving, and railings; purchase of land for current or future use; sitework and associated costs; and

(iv) Equipment and Vehicles to include playground equipment, relocation, and refurbishments and all related costs; buses and other vehicles; equipment, furniture and furnishings, copiers, and other office equipment.”

Superintendent Charles Wilson has shared that if the new ESPLOST resolution is not passed this coming November, the result will be the planned new schools not being built and the General Fund deficit getting worse, because necessary expenditures will be moved back there, instead of the Capital Projects Fund where they are now.

Note that none of these approved uses for ESPLOST include salaries and benefits for BCS employees.

What is the difference between a LOST and an ESPLOST?

Both the LOST and ESPLOST are sales taxes collected in Bulloch County. LOST can go to school operations, unlike ESPLOST, which can only be used for capital purposes (like buildings, buses, and materials).

Both of these sales taxes aim to help offset the cost burden on property owners, and shopping locally directly funds our school system through these local sales taxes.

What is a millage rate?

- The millage rate, made up of mills, is a tax rate. It is multiplied against the assessed value of taxable property in an area to calculate the amount of property tax to be paid.

- Georgia law (OCGA 20-2-165) requires school systems to maintain a minimum equivalent millage rate of 14 mills of maintenance & operations property tax or otherwise lose Equalization Funding which is part of the state funding formula for school systems.

- Currently, one mill of tax is estimated to generate approximately $3.8 million.

- How does the equalization funding work?

Georgia’s equalization grant is intended to close the gap between "high and low property wealth" school systems. This means that areas with lower property values receive more equalization funds. School systems are funded based upon three factors: (1) The difference between the system’s property wealth per student and the state average property wealth per student; (2) The system’s student enrollment; and (3) The system’s property tax millage rate.

- Not only is there a 14-mill minimum requirement, but the state grants more equalization funding to systems with millage rates greater than 14 mills.

- The millage rate is typically set between August and September.

What are the millage rates for recent years?

- Fiscal Year 2025 7.932 (partial rollback)

- Fiscal Year 2024 8.478 (rate increase)

- Fiscal Year 2023 8.263 (partial rollback)

- Fiscal Year 2022 8.568 (full rollback of rate)

- Fiscal Year 2021 8.918 (full rollback)

- Fiscal Year 2020 9.038 (full rollback)

- Fiscal Year 2019 9.427 (full rollback)

- Fiscal Year 2018 9.685 (full rollback)

- Fiscal Year 2017 9.804 (full rollback)

- Fiscal Year 2016 9.848 (no change)

- Fiscal Year 2015 9.848 (full rollback)

- Fiscal Year 2014 9.950 (no change)

How does the school system calculate the millage rate, and what does LOST have to do with it?

- Bulloch County is one of seven counties in Georgia whose county commission gives all or a portion of the local option sales tax revenue (ELOST or Education Local Option Sale Tax) to the school district. Bulloch County Schools receives all of Bulloch County's sales tax, and this satisfies a portion of the state's required 14 mills of tax. See a table here.

- The state required 14-mill millage rate less the imputed value of the local option sales tax millage rate equals the school district’s maintenance and operations property tax millage rate.

- The imputed local option sales tax millage rate is 6.068 mills, as determined from 2023 revenues.

- The state-required 14 mills less 6.068 mills = 7.932 mills, which is the school district's maintenance & operations millage rate for 2024 and a partial rollback. It is currently set to roll back to 7.446 for this year.

- Even though the 7.932 millage rate is lower than the school district's prior year millage rate of 8.478 mills, the rate is still considered a tax increase because it is .374 mills higher than the Bulloch County Board of Assessor's rollback rate of 7.558 mills, based on the annual assessment of taxable property.

The county takes the state-required 14-mill rate and subtracts the assumed value of the LOST, based on previous years' data to get the district's M&O millage rate. In other words, the two amounts work together to meet the required 14-mill rate, better sharing the tax burden amongst property owners and non-property owners.

What brings us to the current budget situation?

In recent meetings, Superintendent Wilson has shared that the BOE expected the $4 million budget shortfall this year (Fiscal Year 26) to balance out next year (Fiscal Year 27). Instead, it has increased by millions of dollars, due to several unexpected financial factors.

The expected shortfall grew from $4 million to an actual $13.2 million for FY26 (creating the expected $15 million shortfall for FY27) due to several things:

- Tax revenue losses of about $1 million: A local decision to implement House Bill 581 (learn more here), offering tax relief for homeowners, is estimated to reduce local property tax collections to Bulloch County Schools by approximately $1 million.

- State funding losses of $7.9 million: Shifts in the state's QBE funding formula (reference the video at the top of the article), particularly related to property tax digest wealth and the "local five mill share" equalization component, have resulted in a significant $7.9 million loss in state funding for the Bulloch county school district this year.

- Big increases in operating costs: The school district is required to contribute a certain percentage to both the Teachers Retirement System and state health benefit plan for its eligible employees. Salaries and benefits make up about 88% of the General Fund expenditures in Bulloch County.

Huge increases in these costs have placed a heavy burden on the district (see examples below). Superintendent Wilson has shared that while the state assists with some of these costs, many locally funded positions, including half of all certified employees in the BCS system, are not fully covered by state funds.

Examples: In FY ‘12, the TRS employer contribution rate was 10.28%; in FY ‘26 it is 21.91%. In FY ‘12, the local annual health insurance employer cost for non-certified employees was approximately $11,400; In FY ‘26 it is approximately $22,800. Over the last several years, BCS has absorbed those cost increases while continuing to roll back the millage rate. The district has also continued to increase pay for teachers to remain competitive but has not raised the property tax rate to cover those increases or that of TRS/health benefits.

- Increases in costs from new improvements to the school district: Bulloch County has made the decision to enhance school safety by adding School Resource Officers (SROs) in all schools. This will cost the system an estimated $0.3 million to $0.8 million this year.

In addition, BCS has increased athletic coaching supplements by half a million dollars, adding to expenses. This money funds increases to athletic supplements for existing middle and high school coaches. This was recommended after an extensive study of Bulloch supplements compared to other similar sized districts in the state and surrounding counties. All head coaches are educators and assistant coaches are employees or lay coaches. Coaches are paid a supplement for the investment of their time in coaching an extracurricular sport.

- Past millage rate rollbacks: The district has continuously rolled back its property tax millage rate, further shrinking available funds.

Superintendent Wilson has described the cumulative effect of these factors as a "domino effect" leading to the current projected $15 million deficit.

Click here to view Superintendent Wilson's full presentation slide deck on these challenges. More detail is also available here.

What's next for Bulloch County Schools?

The reality of the current situation is that a difficult choice has to be made between either increasing the millage rate/property taxes, which increases the existing burden on property owners, or drastically reducing spending on staffing, which includes Reduction In Force (RIF) efforts, eliminating educator jobs in our community and, in turn, affecting the quality of our school system.

At this time, the Board of Education has announced its intention to increase the property taxes it will levy this year by 39.67 percent over the rollback millage rate to prevent the drastic reduction in staffing and decrease the negative impacts on our students.

The BOE plans to increase the millage rate to 10.400 mills, which will increase property tax revenues, and will also still implement cost reductions of over $3 million in the system to try and achieve a balanced budget.

The BOE is required by law to hold three public hearings on this plan, the first of which has already taken place. Two additional hearings will be held this week, both on Thursday, August 21. One hearing is scheduled for 9am, and the other will be held at 6pm. The public is encouraged to attend.